Special Investment Update - March 9, 2026

We have now had a week to observe how global financial markets are responding to the recent military conflict involving Iran. Given the sharp moves across several asset classes, we wanted to provide an update on current investment strategy and forward guidance.

Geopolitical events often create short term volatility, but they also reveal how different asset classes behave under stress. Over the past week, several traditionally defensive areas of the market have behaved somewhat differently than expected, largely due to the surge in the U.S. dollar and the rapid rise in oil prices.

Gold has historically served as a defensive asset class, often rising when stocks decline during periods of geopolitical or economic stress. Over the past week, however, gold has been more negatively affected than usual.

The primary reason has been the strength of the U.S. dollar. A rapidly rising dollar places downward pressure on gold prices, and that relationship has been particularly pronounced during the past week. Based on history, we believe this dynamic to be temporary. Surges in the U.S. dollar are common at the beginning of geopolitical conflicts as investors seek the perceived safety of dollar denominated assets. As the dollar moderates, gold has historically resumed its more typical defensive role within diversified portfolios.

International equities have also declined more than U.S. stocks during the past week. This has had only a modest impact on our portfolios due to our existing underweight allocation to international markets.

Interest rates have also moved higher during the past week as markets react to the potential inflationary implications of rising oil prices. Because bond prices move inversely to interest rates, this has pushed most bond markets into slightly negative territory despite their typical role as a defensive asset class. Short term rate spikes tied to commodity shocks are a well-documented historical pattern.

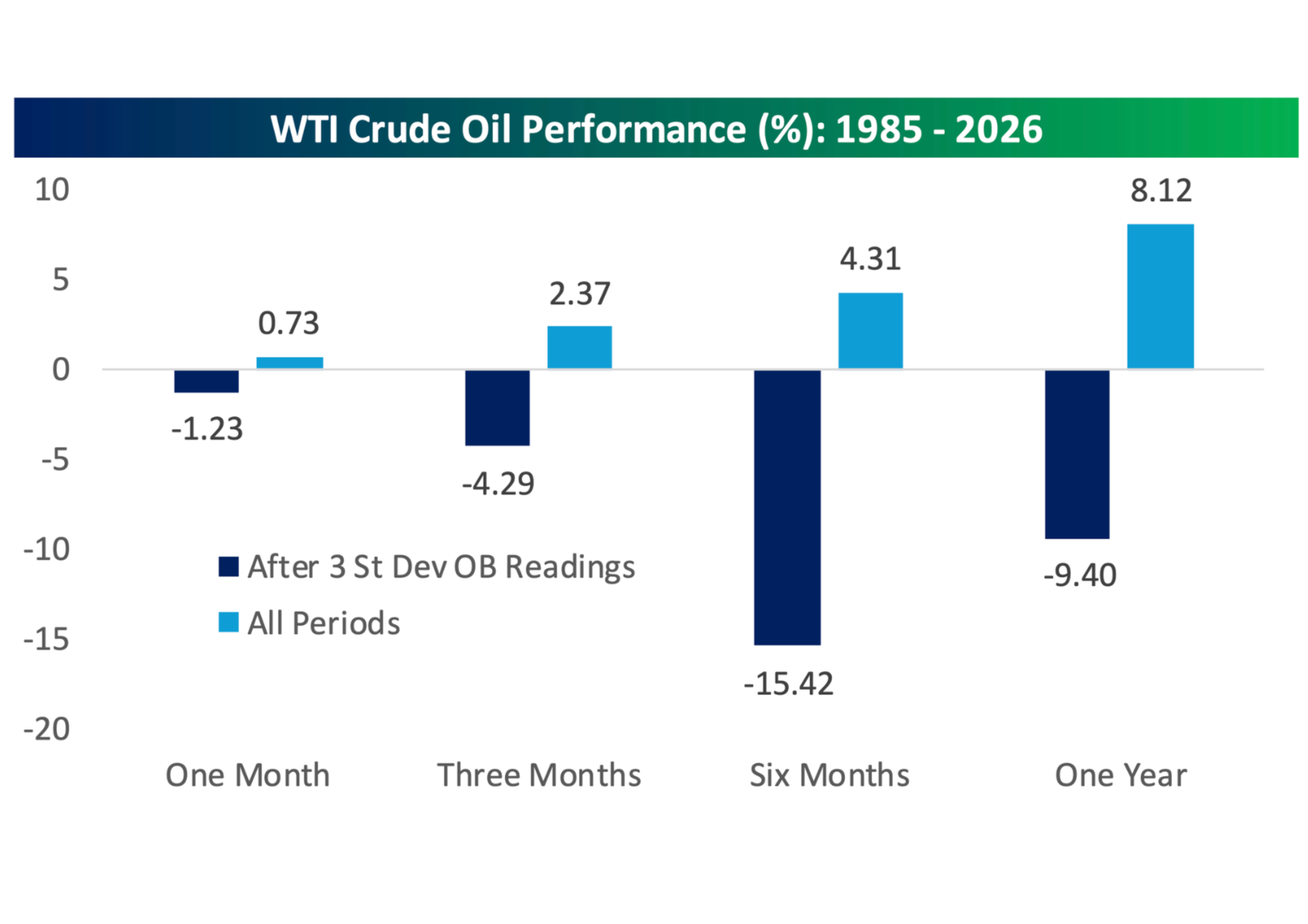

What History Suggests From Oil and Geopolitical Events

Crude oil prices have increased to over $100/bbl the past week. This move represents more than three standard deviations above normal levels and marks the largest weekly gain on record going back to 1985.

However, it is important to note that oil traded above $90 a barrel for most of 2022 after Russia’s Ukraine invasion and exceeded $100 a barrel from 2011 to 2014. Neither price surge led to a recession.

Historically, moves of last week’s magnitude have proven unsustainable. As the chart below illustrates, after previous periods when oil reached similarly extreme overbought levels, prices declined in the months that followed. On average, oil prices fell more than 15% over the subsequent six months:

www.bespokepremium.com (The Bespoke Report March 6th, 2026)

This pattern has important implications for interest rates. If oil prices follow their historical path and begin to decline, inflation pressures should ease and interest rates are likely to follow. In that environment, bond prices would be expected to recover as yields move lower.

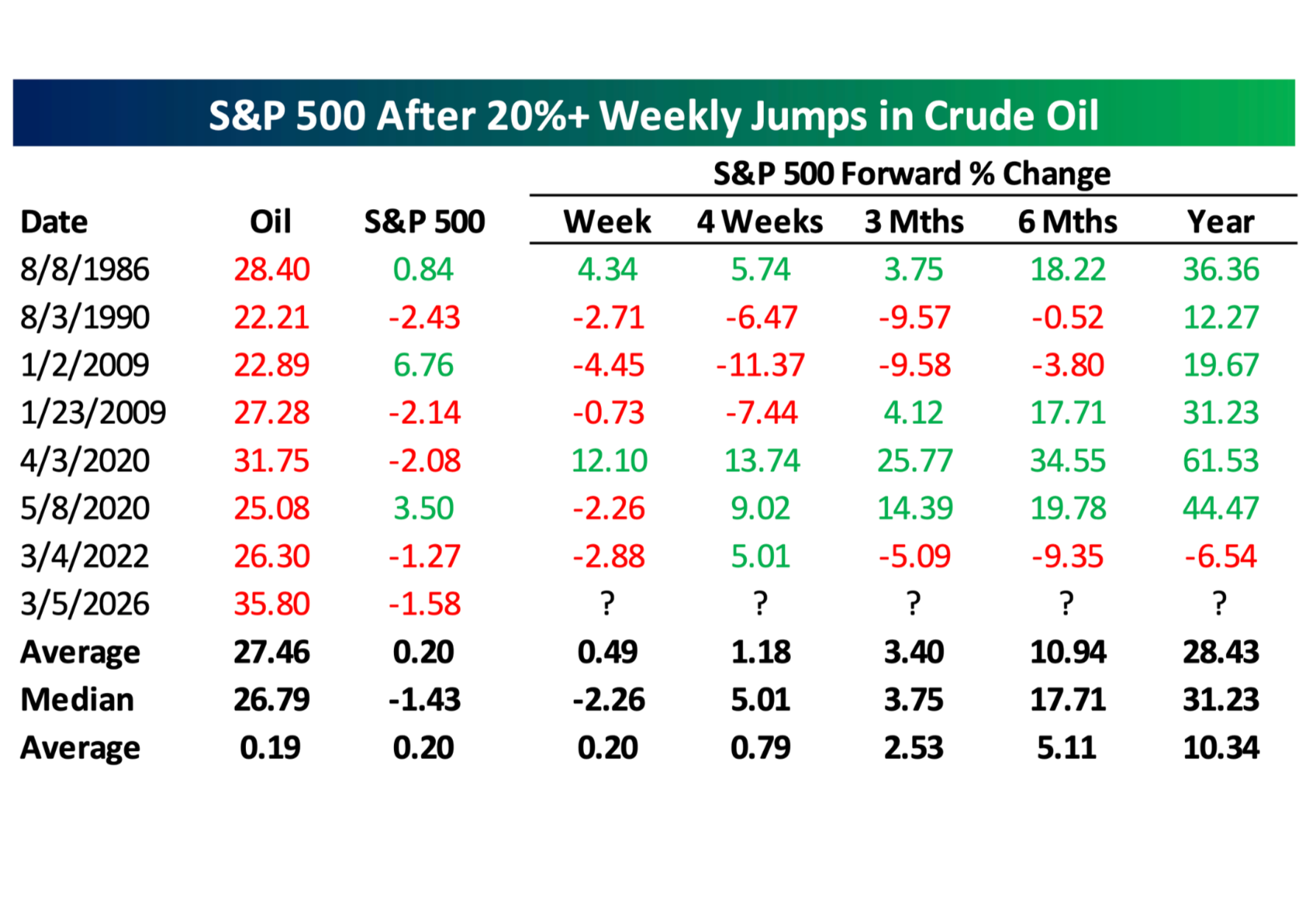

It is also important to understand the relationship between oil prices and equity market performance. The next chart highlights subsequent stock market performance when oil prices increased by more than 20% in a single week:

www.bespokepremium.com (The Bespoke Report March 6th, 2026)

Final Thoughts

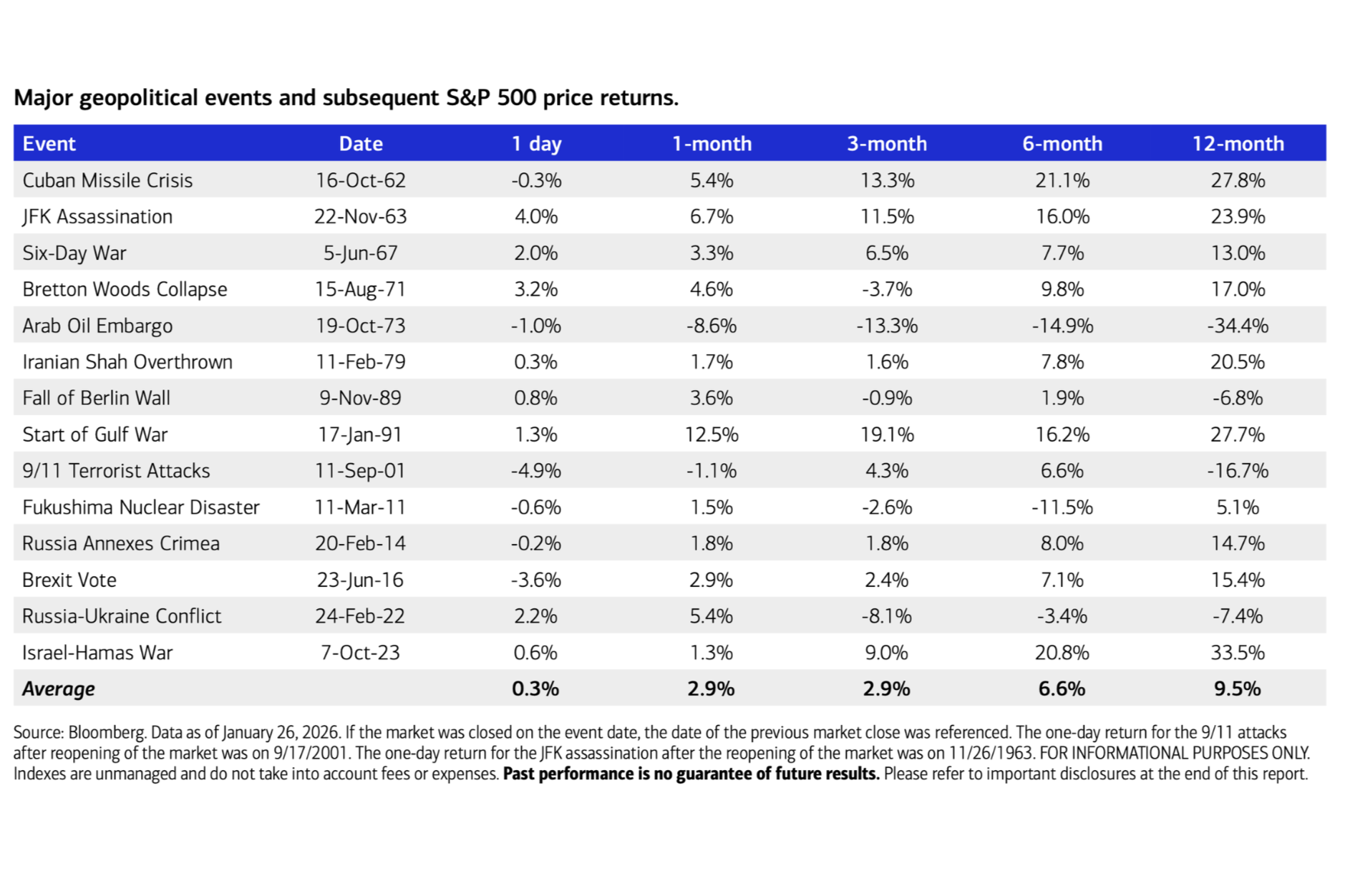

While the stock market has typically been volatile in the immediate aftermath of these spikes, the longer term results have historically been strong. Over the twelve months following these events, the S&P 500 rose six out of seven times, with four of six gains being over 30%! This is a reminder that proper allocation going into these types of geopolitical events (which we feel we have!) allows for patience, i.e. not having to make critical investment decisions in a fast moving market.

The final chart provides a broader perspective by examining past major geopolitical events and the subsequent performance of the S&P 500:

Historically, the U.S. stock market has shown resilience following geopolitical shocks. As show above, across fourteen major geopolitical events, the S&P 500 was higher one year later in eleven cases, with an average twelve month return of approximately 9.5%. Only three of those fourteen periods produced negative returns.

While each situation is unique, the consistent historical takeaway is that markets tend to adjust and recover as uncertainty fades and economic fundamentals reassert themselves.

How We Are Managing Portfolios

In environments like this, we track developments through our Investment Road Signs© framework, which we use to measure market risk and ensure portfolios remain properly positioned.

The goal is not to time the market, but to manage exposure so portfolios can weather downturns while remaining aligned with long-term investment objectives.

The key to this risk management system is to provide guidance for the overall risk level across capital markets, which we viewed as higher than normal, with three out of our five road signs present. Our Investment Road Signs© framework helped us significantly in adding defensive holdings to your portfolio such as gold, high quality bonds, and structured products we refer to as ‘income notes’ and ‘equity hedges’ that have all reduced volatility significantly across client portfolios.

We will continue to monitor developments closely and rely on our Investment Road Signs© to guide decisions regarding the appropriate level of risk in the current investment environment.

Robert Amato, CFP®, CIMA®

Principal

--------

This article may not be copied, reproduced, or distributed without Compass Wealth Management’s prior written consent. Compass Wealth Management is a Registered Investment Advisor. Advisory services are only offered to clients or prospective clients where Compass Wealth Management and its representatives are properly licensed or exempt from licensure. This article is solely for informational purposes and is not intended to be relied on as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Compass Wealth Management to be reliable, are not necessarily all-inclusive, and are not guaranteed as to accuracy. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. Investments involve risks.